Many companies are busy operating and often do not have, or take, the time to conduct a review of expenses. However, a yearly review can be quite helpful to the bottom line.

By Julie Murphy

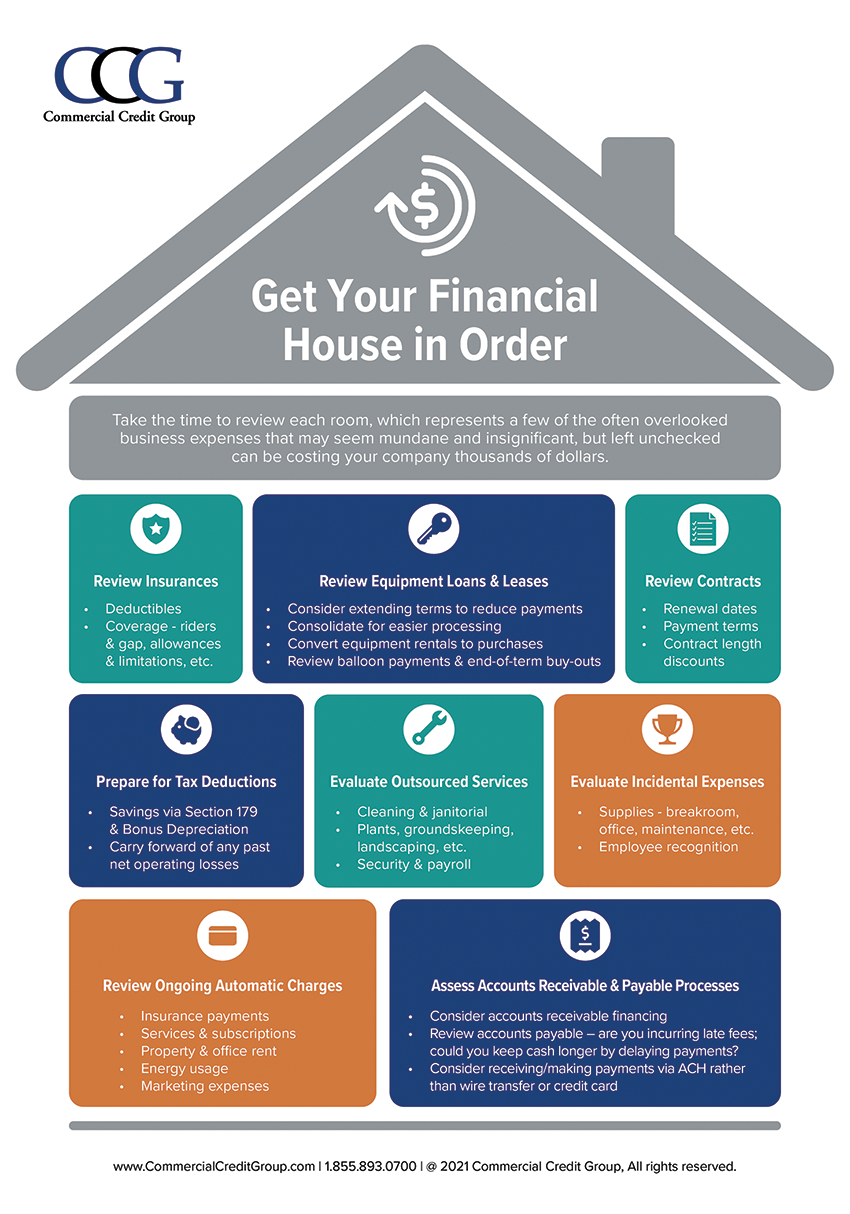

When was the last time you sat down and thoroughly reviewed all your business expenses? Sure, you close your books each month end, review your basic financial statements (income statement, balance sheet, etc.), and file your taxes each year. However, have you ever really looked at and evaluated all of the often overlooked business expenses that may seem mundane and insignificant? Left unchecked these can be costing your company thousands of dollars.

Review Any Ongoing Automatic Charges

In this day and age of electronic billing and electronic payments, it is easy to set up automatic payments for recurring charges. While helpful to ensure you do not miss payment deadlines, it is also easy to forget about these charges, even if you are not actually using the services any longer. Many bank payment platforms now have easy filters to help identify ongoing, recurring charges:

• Insurance payments—healthcare, liability, equipment and ve hicle coverage, property, unemployment, cyber threat, etc.

• Maintenance fees

• Services and subscriptions

• Property and office rent

• Energy usage

• Website and other marketing expenses

Review Insurance Coverages

Similar to automatic charges, it is easy to adopt a ‘set-it and forget-it’ mentality when it comes to insurance. You simply renew your existing policies. Your business inevitably changes each year, so it is important to review your policies to ensure that you have the appropriate coverage for your business operations. This applies to all your insurance policies (healthcare, vehicle, general liability, etc.) and your insurance agent can help with this review process and the associated risk assessments:

• Deductibles

• Coverage allowances and limitations

• Riders and gap coverage

Evaluate Outsourced Services

Using outsourced services is a good way to keep employee headcount and benefits payments low. Circumstances and conditions change, so it is a good idea to evaluate the services and contract terms on a regular basis. Additionally, sometimes it makes sense to bring currently outsourced services in-house:

• Cleaning and janitorial

• Groundskeeping, landscaping, plant maintenance

• Security

• Payroll

Review Equipment Loans and Leases

If you have financed or leased equipment, especially if you have multiple pieces and several loans or leases, a regular evaluation of these is recommended. Many leases come with balloon payments or end-of-term buy-outs that can be quite high, so you need to plan ahead to ensure you have the cash to make those payments. Oftentimes, loans can be consolidated to help reduce monthly payments and simplify processing:

• Consider extending terms to reduce monthly payments

• Consolidate for easier processing

• Convert rentals to purchases to reduce monthly payments and potentially take advantage of Bonus Depreciation for tax purposes

• Review for balloon payments or end-of-term buy-outs

Assess Accounts Receivable and Accounts Payable Processes

Discounted payment terms can have a big effect on cash flow, both from an accounts receivable and accounts payable standpoint. Additionally, ancillary charges, such as wire charges and credit card fees, can impact the bottom line:

• Consider accounts receivable financing to get payment for your invoices faster, thus enhancing cash flow (AR financing is only available for invoices issues to other companies, so it is not an option for hauling companies that have only residential contracts)

• Review accounts payable processes—are you incurring any late fees due to delayed payments; could you keep your cash longer by delaying payments?

• Consider receiving/making payments via ACH rather than wire transfer or credit card

Review Contracts

Similar to ongoing automatic charges, it can be easy to overlook contract terms such as automatic renewal dates and notification deadlines. In some cases, you may no longer need a service, but if you miss the renewal notification deadline, you could be locked in for another term without even realizing it.

It is also important to evaluate usage of the service to ensure that you are not paying for more than what you are using. For example, many software contracts are based on the number of seats, or users, and if your staff has changed, you may be paying for more seats than are being used. Consider payment terms and contract length discounts. Some services offer discounts for upfront payments, automatic billing, or extended contract terms. Be sure to ask about any available discounts or current promotional pricing:

• Check renewal dates

• Compare usage to contract terms

• Evaluate payment terms and contract length discounts

Prepare for Tax Deductions

Consult with your tax attorney or tax preparer to review possible tax deductions. These could be related to equipment purchases (Section 179 and Bonus Depreciation), net operating losses, and any number of other tax items. Especially with the various tax changes and loans related to COVID relief. This year it is especially important to fully review your options:

• Section 179 and Bonus Depreciation

• Carry forward of any previous net operating losses (NOL)

Evaluate Incidental Expenses

Incidental expenses, while typically small, can add up over time. Some can be paid for out of a petty cash account which can make them harder to track:

• Supplies—office, breakroom, maintenance, etc.

• Employee recognition

Your Bottom Line

In general, many companies are simply busy operating and often do not have, or take, the time to conduct this type of review of expenses. However, a yearly review can be quite helpful to the bottom line. | WA

Julie Murphy is the VP of Marketing for Commercial Credit Group Inc. Julie has two business degrees, but learned about budgeting and household finance from her parents. She has managed budgets as high as $6 million and absolutely hates to waste money. She joined CCG in 2016. Julie can be reached at jmurphy@

commercialcreditgroup.com.

Note: This article first appeared on the CCG equipment financing blog.