Renewable Energy

The Shifting Landscape for Renewable Energy in the UK

Considering how changes in policy and technology preference are resulting in significant shifts in the development of waste derived renewable energy projects in the UK.

Euston Ling and Dr. Adam Read

The UK Government has a commitment to reduce the UK’s greenhouse gas emissions by at least 80 per cent by 2050 (from 1990 levels). As a result, the UK landscape surrounding renewable energy is shifting rapidly to help deliver a low carbon future. Recently, there have been a number of national consultations which are likely to have a significant bearing on the future viability of non-fossil fuel based energy provision including a number of planned energy-from-waste (EfW) projects. Schemes which enable the heat produced during the electricity generation process to be captured and distributed via a district heating network, i.e. combined heat and power (CHP), are being given increasing focus and prioritization. From a local perspective, proposed local changes such as those put forward by the Mayor of London to realize greater uptake of decentralized energy systems through advanced conversion technologies, have added further complexity to this shifting landscape.

While the uptake of CHP has been slow in the UK, progress is being made with the recent financial close of a major EfW project in South West Devon. Subject to planning consent, this contract will see German company MVV Umwelt build, operate and maintain a CHP facility in the North Yard of the Devonport naval base in Plymouth. Taking in 245,000 tons of residual waste a year, the company will supply steam and electricity to the naval base under a 25-year energy services agreement with the Ministry of Defense. In order to realize CHP opportunities, the following key factors need to be in place:

-

CHP enabled EfW infrastructure (currently not common in the UK);

-

Heat distribution network(s);

-

Sufficient and predictable heat “baseload”—constant heat demand load;

-

Energy prices (for heat and electricity) which are able to cover the long term infrastructure costs.

Supporting CHP Infrastructure

Until recently, the market was not supportive of CHP systems because of the costs of retrofitting pipework into the urban environment and the costs of altering existing EfW facilities to enable heat off-take. But with increasing concerns about the need for new waste infrastructure to meet EU Landfill Directive targets, worries about energy security and UK government commitments to the growth of renewable energy generation a great deal of central government focus has been on how to stimulate this market.

There are two key incentives which are intended to support long-term stable heat prices in an effort to support the viability of CHP infrastructure in the UK. These are the Renewables Obligations Certificates (ROCs) and the soon to be launched Renewable Heat Incentives (RHIs).

Renewables Obligation

Under the current Renewables Obligation (RO), support for large scale renewable electricity projects will be provided for up to 20 years, and will run until 2037. Here, ROCs are able to be claimed for the biomass fraction of waste which for EfW schemes which are accredited under the CHP Quality Assurance (CHPQA) scheme until March 31, 2017 when the RO will be “vintaged” or no longer open to new accreditations. Presently, the number of ROCs which are able to be claimed for EfW projects is dependent upon “banding levels” which have been set according to generation type such as Energy from Waste with CHP (1 ROC), Gasification/Pyrolysis (2 ROCs) and Anaerobic Digestion (2 ROCs).1 A review of banding levels is expected to be completed in the third quarter of 2011. For 2010/11, the buy-out price for ROCs was £36.99 (about $60) and will be updated annually to reflect changes in the Retail Prices Index.2

Renewable heat is seen as a key way in which the UK can meet its renewable energy targets. Accordingly, in March 2011, the UK Government announced details of the Renewable Heat Incentive with the aim of having the underpinning regulations approved by Parliament in the summer of 2011. This scheme will be introduced in two phases with the first being a long-term (20 year) tariff to support non-domestic (industrial, commercial and public) sectors in 2011, and the second for the domestic sector to be introduced in late 2012.

In 2011, eligible solid recovered fuel (SRF) in the RHI will be limited to SRF from municipal solid waste (MSW) and SRF waste streams containing no more than 10 per cent fossil fuel. For medium scale CHP schemes firing MSW, support will range from £19 to £47/MWh (about $31 – $76). For large scale CHP schemes, the tariff will be set at £26/MWh (about $42).3

It should be noted that after April 1, 2013, it is likely that heat from EfW CHP schemes will no longer be rewarded through the RO but instead through the RHI, meaning that CHPQA qualification would no long be required as support would be provided directly on the used renewable heat output of a facility. Therefore, while accreditation under the RO will be available until March 31, 2017, the interaction between the incentives for renewable heat and electricity is as yet unclear.

However, what is certain is that these two schemes will not only encourage greater delivery of renewable energy solutions, but more importantly will offer the waste sector a viable and attractive end point for materials collected from households and businesses.

Calculating Energy Output

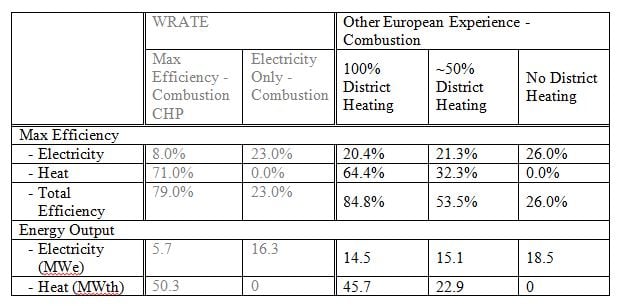

In 2010, a study was conducted on a number of EfW systems as part of a study for the Welsh Assembly Government. This study used lifecycle software to model waste management systems, including conventional combustion, gasification with steam, and gasification with gas turbines to determine what thermal efficiency targets should be set for future energy EfW facilities in Wales.

Traditional waste to electricity facilities in the UK have thermal efficiencies of under 30 percent and the Welsh Government as part of their commitment to sustainable development wanted to set a higher threshold to drive cleaner energy production from waste streams. The results of this study were used to calculate the energy output from a facility taking 153,000 tons of Solid Recovered Fuel from waste sources (SRF) with a calorific value of 13MJ/kg over an annual period of 7,800 hours. These results were then compared with in-house European experience provided in Captions. Here, it was found that the modelled efficiency is lower than the calculated efficiency from European facilities in part due to the following reasons:

-

Very limited data from EfW facilities operating in full CHP mode within the UK;

-

Varying system boundaries; and

-

Different input composition.

Notwithstanding the differences in results, what they do point to is a maximum overall efficiency around 80 percent, with the vast majority of energy being supplied as heat. The other lesson to be drawn is that electricity should always be generated to make use of the high quality heat (typically around 400°C and 40 bar) with a heat off-take scheme to provide the base-load for “mopping up” as much of the lower quality energy as possible, thereby maximising the overall energy efficiency.

If the above scheme were eligible for both electricity incentives and heat incentives (although there is uncertainty as to whether this will be the case), the additional income would be substantial. However, one of the main cost drivers for any district heating networks relates to the installation of the pipe network for hot water. Here, the Department for Energy and Climate Change (DECC) have estimated that the cost to install the distribution network is in the order of £1,000 (about $1,630) per meter with hard dig (installation along roads and pavements) being 25 percent more expensive, and soft dig (installation along riverbanks and fields) being 25 percent cheaper.4

Supporting the Co-Location and End Users

In parallel to improving thermal efficiencies and the delivery of greater renewable energy and heat, there is a need to support the co-location of EfW facilities and end users of heat and energy to ensure there is no loss of either in transit. As such we are starting to see the development of Eco Parks where waste materials are processed to generate heat which are used to power large-scale warehouse, refrigeration or steaming facilities. This trend is likely to gather pace in the coming years and a number of the UK’s largest supermarkets are already doing this at their regional distribution centres as they have the waste streams and the heat load requirements at one location.

In order for the shift towards CHP and district heating to continue, there is a clear need for robust and effective renewable incentives, and the UK Government will be monitoring its policies and incentive programmes closely to determine their success in the coming 18 months.

Dr. Adam Read is Global Practice Director for AEA’s Resource Efficiency and Waste Management Practice. He has had more than 17 years of operational experience both in the UK and overseas, the last 10 in consultancy. He was awarded an honorary professorship in 2002 for his pioneering work on waste communications and public engagement. He is a Fellow of the Royal Geographical Society and a Fellow of the Chartered Institution of Wastes Management. Adam leads a team of waste and resource management consultants at AEA specializing in resource efficiency, product design, clean technologies, waste management strategy, recycling service design, technology appraisal, procurement, training and behavior change. He is recognized as a leading waste management thinker with an extensive portfolio of research papers, conference articles and collaborative investigations both in the UK, U.S. and Europe. He can be reached at 07968 707 239 or e-mail [email protected].

Euston Ling is AEA’s Knowledge Leader for Waste Technologies and Modelling, leading a business unit with a number of technical specialists on high level technology assignments for UK Government and Local Authorities, including carbon footprints, lifecycle analysis and carbon metrics. Euston is currently on secondment to the North London Waste Authority as their Fuel Procurement Manager. Euston has been a consultant for the last 10 years and was previously involved in all aspects of waste management at the Sydney Olympics. He can be reached at 07968 707 249 or via e-mail at [email protected].

Notes

1. Department of Energy & Climate Change (2011), http://chp.decc.gov.uk/cms/roc-banding/

2. Ofgem (2010), www.ofgem.gov.uk/Media/PressRel/Documents1/RO%20Buy-Out%20price%202010%2011%20FINAL%20FINAL.pdf

3. Department of Energy & Climate Change (2011), www.decc.gov.uk/en/content/cms/what_we_do/uk_supply/energy_mix/renewable/policy/incentive/incentive.aspx

4. Department of Energy & Climate Change (2010), http://chp.decc.gov.uk/cms/workshops/

Table 1

Potential EfW efficiencies.

Table courtesy of AEA.

Case Study

North London Waste Authority

With energy security and carbon impacts becoming increasingly important, it is vital for the UK to secure more affordable, low-carbon energy efficient solutions. Moreover, such solutions must deliver the best possible environmental, financial and commercial outcomes. The North London Waste Authority (NLWA)—which covers 7 London Boroughs and 1.7 million residents—has decided that this can be achieved through projects where fuel (SRF produced from 850,000 tpa of waste risings in the authority) are delivered to locations where an energy demand already exists, rather than seeking to attract energy users to develop an energy-from-waste (EfW) facility. Accordingly, the NLWA is seeking to procure two contracts: the first to produce a Solid Recovered Fuel (SRF) from municipal waste and the second for the use of the resultant SRF.

By seeking to produce around 300ktpa of SRF with a CV of 13MJ/kg and a biomass content of 50 percent, the Authority has attracted a much wider market interest than had they been looking only at EfW providers, ranging from large-scale industrial energy users and producers to smaller combined heat and power (CHP) schemes, which otherwise may have been excluded from a procurement of this nature.

By deliberately allowing the market to site a fuel use facility away from the waste processing services, the Authority is hopeful that the emerging solutions will deliver much greater CHP and thus improve the thermal efficiency of the entire system, underpinned by secure long term heat demand to take advantage of ROCs and the new RHI. Assuming a solution with a modest electrical efficiency of 25 percent and a heat efficiency of 25 percent, this could see a substantial benefit to the authority by providing an additional £18.50 /MWh (about $30) of electricity and £13/MWh (about $21) of heat generated by the project depending upon the outcomes of the Electricity Market Reform Consultation, thereby reducing the overall cost of waste management to residents and helping to deliver the UK’s carbon and energy ambitions.