Conrad Nichols

Managing the sustainability of Li-ion batteries at end-of-life (EOL) will continue to become increasingly important as the demand for Li-ion batteries continues to grow in sectors such as electric vehicles, stationary energy storage, and consumer electronics. Recyclers will aim to extract valuable metals, and battery manufacturers will hope to use recycled materials in new battery manufacturing. This will help minimize these materials’ supply chain risk, and help manufacturers shield themselves from fluctuating raw material prices. Importantly, another key driver that will push Li-ion recycling market growth is policies being enforced in key regions.

This article draws insights from IDTechEx’s report “Li-ion Battery Recycling 2023-20437”. While China has some of the more extensive policies regarding Li-ion battery recycling and end-of-life management, policies and regulations being implemented in the EU and India will contribute to Li-ion battery recycling market growth in these regions.

EU Battery Regulation

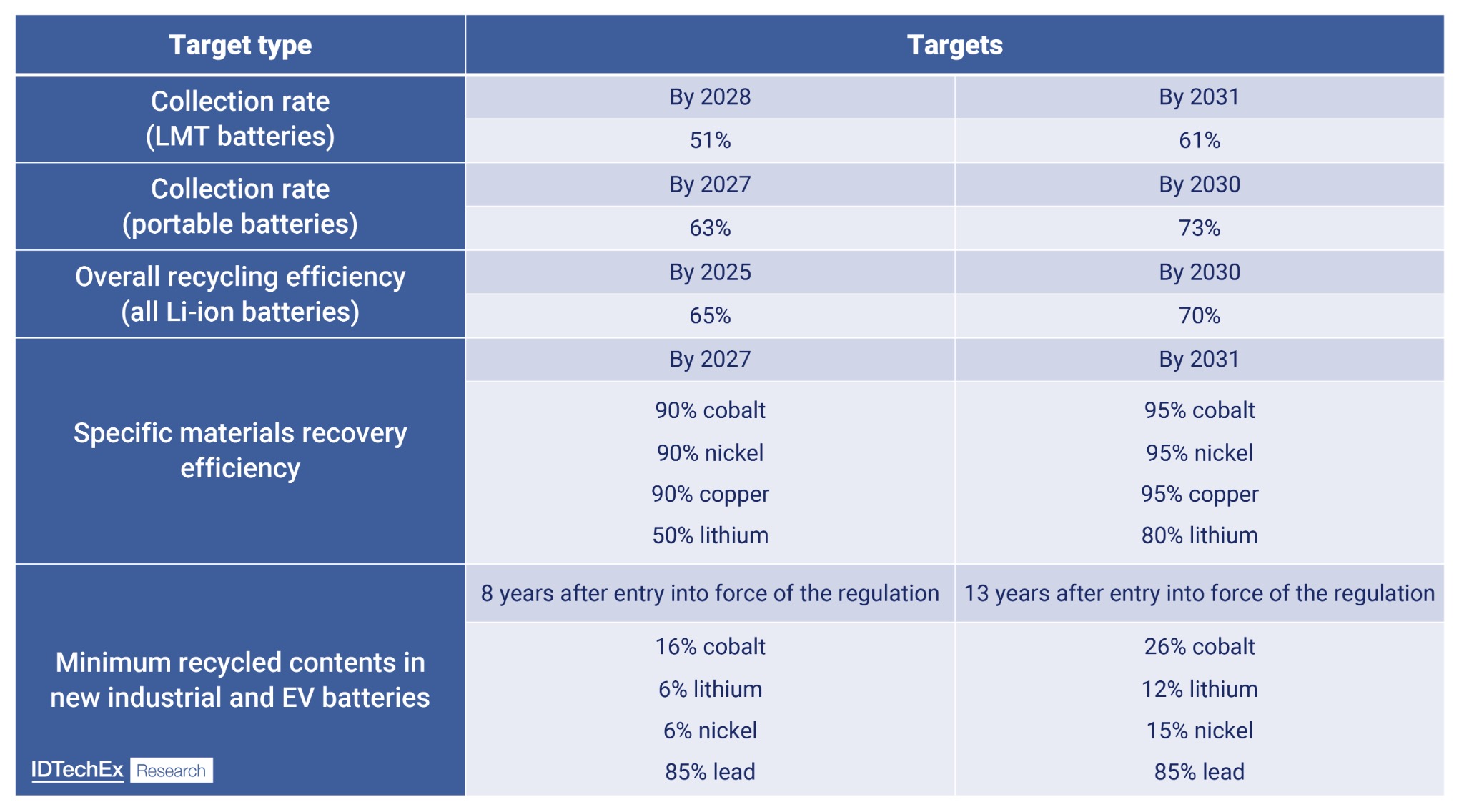

The EU Battery Regulation will enforce new specific collection rate targets for light means of transport (LMT) and portable batteries. These are important targets, as the collection of consumer batteries has not been greatly incentivized or well achieved in the past. The Commission plans to assess the feasibility of deposit schemes for portable batteries by the end of 2023. Also included in the Regulation are specific material recovery efficiency targets for all Li-ion batteries and minimum recycled contents targets in new EV and industrial batteries. These targets are summarized below.

In 2023, the EU compiled the fifth version of their critical raw materials list. These are defined as being of high economic importance and at risk of supply disruption. Key materials on this list used in batteries include lithium, cobalt, manganese, natural graphite, and aluminum. While nickel and copper are not on the list, they are still listed as strategic raw materials and potentially subject to future supply risks. The targets specified above could help reduce supply risk through domesticating the supply of lithium, nickel, and cobalt from recycling in the EU.

India Battery Waste Management Rules 2022

India introduced its ‘Battery Waste Management Rules 2022’, replacing the ‘Batteries (Management and Handling) Rules, 2001’. This will cover electric vehicle, portable, and industrial batteries. These are rules based on the Extended Producer Responsibility mandate, where battery producers are responsible for the collection and recycling/refurbishment of retired batteries. Similar to the EU Battery Regulation, these rules specify targets for specific material recovery efficiency targets in EV batteries, but also for portable and industrial batteries. Targets are also specified for battery collection rates across these sectors and minimum percentages of recycled materials to be used in new EV and industrial batteries.

Potential Incentives in the US

The US does not see any strict policies regarding Li-ion battery recycling. However, through the Inflation Reduction Act (IRA), EV battery manufacturers may be eligible for an Advanced Manufacturing Production (PTC) credit. This specifies that a minimum percentage, by value, of critical raw minerals are extracted or processed in the US, from a country with a free-trade agreement with the US, or recycled in North America. This minimum percentage is 40% until the end of 2023, increasing year-on-year until 1 January 2027, where this percentage is 80%. If this requirement is met, a battery producer would be eligible for a US$3,750 PTC. Therefore, EV battery manufacturers will be keen to source more battery materials domestically, which could come from US recyclers.

The IRA details 50 critical minerals, but the most relevant for batteries are aluminum, cobalt, graphite, lithium, manganese, and nickel. In July 2023, the US Department of Energy (DOE) also released an updated critical materials assessment report. Lithium, nickel, cobalt, and graphite were identified as critical materials in the medium term (2025-2035). However, sourcing minerals produced from recycling on a large scale in North America over the next few years is unlikely. This is due to the lack of commercial-scale hydrometallurgical recycling plants in this region, though players are looking to expand their hydrometallurgical capacities. For example, Li-Cycle is one of the few players planning to establish a commercial-scale hydrometallurgy plant in the US. Hydrometallurgical recycling offers the production of battery-grade metal salts, which can be further processed into precursor for new battery cathodes. Due to the lack of current hydrometallurgical recycling capacity in the US, it is unlikely that EV battery manufacturers will be able to make great use of the PTC being offered, at least in the short term.

Concluding Remarks

China, the EU, and India’s policies will help to drive growth of the Li-ion battery recycling market in these regions. Incentives in the US could drive demand for recycled material, but deployment of the necessary recycling infrastructure is still lacking. Other regions that see great Li-ion battery demand, such as Japan, South Korea, and Australia, do not have strict policies regarding Li-ion battery recycling. Therefore, Li-ion battery recycling market growth in these regions will instead be driven by other market-wide factors. This includes battery manufacturers looking to use recycled battery materials in new battery manufacturing, helping to minimize dependence on raw materials and shielding themselves from fluctuating raw material prices and supply risks. These factors will also continue contributing to growth in regions where new regulations and policies are being introduced.

For more on technologies, key players, policies, economics and granular 20-year recycling market forecasts, refer to IDTechEx’s latest report “Li-ion Battery Recycling Market 2023-2043”. For more information on the report, including downloadable sample pages, visit www.IDTechEx.com/LiRecycling. For the full portfolio of energy storage reports available from IDTechEx, please visit www.IDTechEx.com/Research/Energy.